In 1966, Laffer’s Stanford Ph.D. adviser Emile Despres, and Robert Mundell’s adviser from his 1956 MIT Ph.D. Charles Kindleberger, wrote a piece (with Walter Salant of the Brookings Institution) on the apparent crisis concerning the balance of payments, fixed exchange rates, and the gold standard. They saw the perception of a crisis as much ado about nothing. “The Dollar and World Liquidity appeared in The Economist, which called the piece “a minority view.”

The majority view, adhered to by The Economist, was that of Triffin. American trading partners were piling up far more dollars in their own bank and reserve accounts for the United States ever to have enough gold in the event of mass redemption requests (again, the dollar was the one key currency at the time redeemable on demand to foreign monetary authorities in gold, at $35 per ounce). Because global gold production could not match global dollar demand, and because foreigners had an inordinate demand for dollars, the system was headed for crisis. There would be a huge run on the dollar at some point as foreigners tried to get gold before the inevitable official American increase in the price of gold so that gold supply was a closer match to foreign-held dollars outstanding.

Laffer and Mundell’s advisers told everyone to cool it. They said that foreigners wanted dollars for all sorts of good reasons – they wanted to invest with them, for example. The American gold stock did not have to keep up with the foreign dollar stock. If there was healthy economic return to investment, people abroad would prefer to use their dollars on things other than gold (if not simply keep their dollars banked and earning interest). Foreigners were not disposed to hoard gold, because they needed the flexibility to make investments when they wished. The United States having a very demanded currency the world over was no reason to think the gold standard was not working very well.

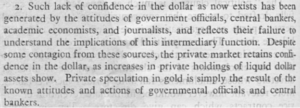

In the telling passage marked “2.”, Despres, Kindleberger, and Salant noted that the whipping up of concern of the untenability of the dollar against gold had come from non-businesspeople, academics, government officials and the like. The very provenance of the crying of crisis over the dollar and gold—it came from non-real-economy sources—was a sign to these economists that the crisis was a manufactured one.